Picture this: it’s the end of the month, and you’re staring at your bank statement wondering where the money went. It’s a familiar, frustrating feeling. Managing money often feels like a second job—one that involves spreadsheets, guilt, and a lot of “I shouldn’t have bought that.”

But what if you could simplify the whole thing?

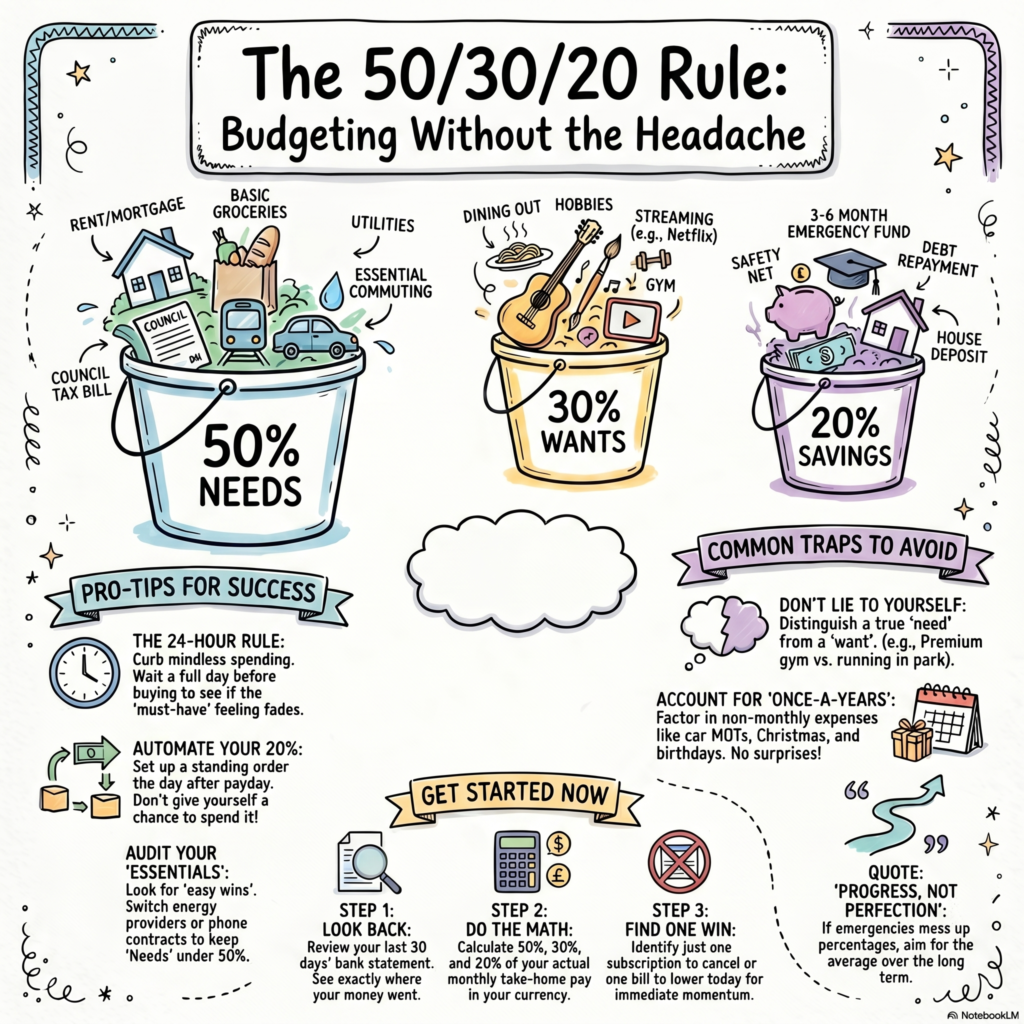

That’s where the 50/30/20 rule comes in. It’s not a complex accounting system; it’s a straightforward way to split your income that takes the guesswork out of your spending. No spreadsheets required—just a bit of honesty and three simple “buckets” for your cash.

By the end of this, you’ll have a clear roadmap for your money that actually leaves room for you to enjoy your life.

What Exactly is the 50/30/20 Rule?

The beauty of this system is the math is already done for you. You take your monthly “take-home” pay (what actually hits your bank account after tax) and divide it like this:

- 50% for Needs: The non-negotiables. Rent, bills, and groceries.

- 30% for Wants: The fun stuff. Dining out, hobbies, and that Netflix sub.

- 20% for Savings: Your future self. Emergency funds and debt clearing.

If you bring home $2,000 a month, that means $1,000 for the basics, $600 for the fun stuff, and $400 for your savings.

The reason this works so well is that it gives you permission to spend. If you’ve stayed within your 30%, you can grab that extra coffee or go to the cinema without that nagging voice in your head telling you that you’re “failing” at adulting.

The 50%: Handling the “Must-Haves”

This category is for anything that keeps your life running. If you stopped paying these, things would go south pretty quickly. We’re talking:

- Rent or mortgage and Council Tax

- Gas, electric, and water

- Basic groceries (not the fancy organic treats)

- Commuting costs and car insurance

The trick here is being ruthless about the word “essential.” If your “needs” are creeping past 50%, don’t panic. It happens—especially with the current cost of living. Usually, the easiest wins are in the things we forget to check. When was the last time you switched energy providers or looked for a cheaper phone contract? Even a £20 saving here and there adds up to a lot over a year.

The 30%: Spending Without the Guilt

This is the part most budgets get wrong. They try to cut out “fun” entirely, which is why people give up. With 50/30/20, your lifestyle is baked into the plan.

This covers your social life, gym memberships, holidays, and clothes. The goal isn’t to stop spending; it’s to stop mindless spending.

My Favourite Trick: If you’re a big online shopper, try the “24-hour rule.” Put that £60 jacket in your basket, but don’t hit buy. If you still want it 24 hours later, go for it. You’ll be amazed how often that “must-have” feeling disappears by breakfast the next day.

The 20%: Your Financial Safety Net

This is the 20% that changes everything. It’s your emergency fund, your house deposit, or your “I’m quitting my job” fund.

The goal is to build a 3-to-6-month buffer of your essential expenses. If your “needs” cost $1,000 a month, aim for a $3,000 cushion. It sounds like a lot, but if you’re tucking away $400 a month, you’re there in less than a year.

Pro Tip: Treat this 20% like a bill you have to pay. Set up a standing order for the day after payday so the money moves before you even have a chance to miss it. If you can’t see it, you won’t spend it.

Where Most People Trip Up

Even with a simple rule, there are a few common traps:

- Lying to yourself: Calling a premium gym membership a “need” when a pair of running shoes and a park would do the same job.

- Forgetting the “Once-a-Years”: Car MOTs, Christmas, and birthday gifts aren’t surprises—they happen every year. Factor them in.

- Being too perfect: Some months, your car will break down or a friend will get married. Your percentages will get messy. That’s fine. Just aim for the average to be right over the long term.

Making It Work for Your Life

Numbers on a page are great, but life isn’t a textbook. You can (and should) tweak this to fit your reality:

- Aggressive Debt? Move to 50/20/30 and put that extra 10% toward clearing high-interest credit cards.

- High Rent? If you live in a city like London, your rent might eat up 60% of your income. That just means your “wants” have to lean a little thinner for a while.

Everything is a trade-off. The 50/30/20 rule just helps you see exactly what you’re trading.

How to Start Today (Like, Right Now)

Don’t wait for the first of the month.

- Look at your last 30 days: Where did the money go?

- Do the Math: What is 50, 30, and 20% of your actual take-home pay?

- Find One Win: Can you cancel one subscription or find one bill to lower?

Budgeting isn’t about restriction; it’s about intention. It’s about making sure your money goes to the things that actually make your life better. Your future self will be very, very glad you started today.

Ready to see where you stand? Work out your breakdown right now—you might be surprised at how much control you actually have!

Disclaimer: The content on this site is for informational and entertainment

purposes only. It consists of general money-saving tips and lifestyle hacks.

Nothing on this site constitutes financial, investment, tax, or legal advice.

Always do your own research and, where appropriate, seek advice from a qualified

financial adviser before making any financial decisions.